Running a small business in Inland Southern California is challenging enough without falling victim to predatory lenders. When cash flow gets tight and bills pile up, it’s tempting to grab the first loan offer that promises fast money with minimal paperwork. However, these “easy” loans often come with hidden costs that can destroy your business faster than you can say “high interest rate.”

At the Microenterprise Collaborative, we’ve seen too many business owners learn this lesson the hard way. The good news? With the right knowledge and approach, you can secure legitimate funding while protecting your business from financial predators.

Don’t Let Desperation Lead You to a Bad Deal

When you’re struggling to make payroll or cover rent, every lender starts to look like a lifesaver. But research from our partners shows that businesses who rush into bad loan agreements often face:

- Annual percentage rates exceeding 200% on merchant cash advances

- Daily or weekly payment schedules that crush cash flow

- Personal guarantees that put your home and personal assets at risk

- Hidden fees that add thousands to your total cost

- Balloon payments that can bankrupt your business

The COVID-19 pandemic highlighted just how vulnerable small businesses can be. In our 2021 research study, we found that businesses with poor financial records were the most likely to fall victim to predatory lending practices when seeking emergency funding.

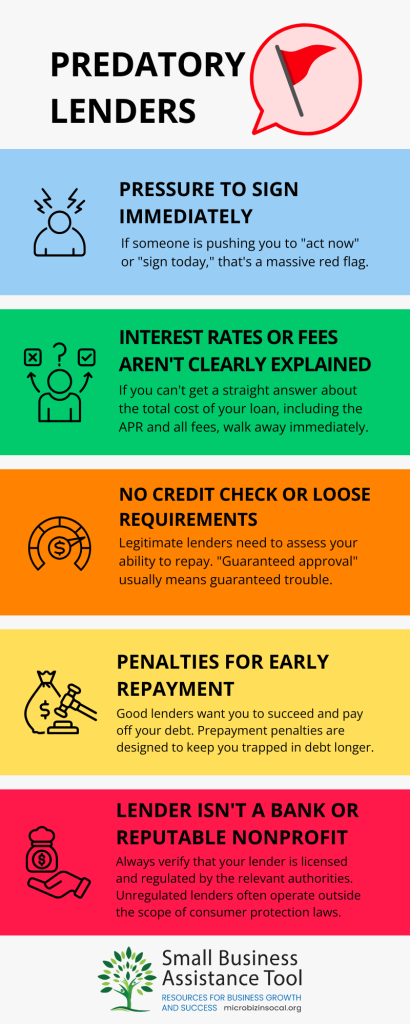

5 Red Flags That Should Make You Run

Before you sign anything, watch out for these warning signs that scream “predatory lender”:

- Pressure to Sign Immediately

Legitimate lenders understand that taking on debt is a major business decision. If someone is pushing you to “act now” or “sign today,” that’s a massive red flag. - Interest Rates or Fees Aren’t Clearly Explained

If you can’t get a straight answer about the total cost of your loan, including the APR and all fees, walk away immediately. - No Credit Check or Impossibly Loose Requirement

While this might seem appealing, legitimate lenders need to assess your ability to repay. “Guaranteed approval” usually means guaranteed trouble. - Penalties for Early Repayment

Good lenders want you to succeed and pay off your debt. Prepayment penalties are designed to keep you trapped in debt longer. - The Lender Isn’t a Bank or Reputable Nonprofit

Always verify that your lender is licensed and regulated by the relevant authorities. Unregulated lenders often operate outside the scope of consumer protection laws.

If you spot any of these red flags, take a step back and get advice before signing anything.

Your Three-Step Strategy for Finding Legitimate Funding

Instead of falling into predatory lending traps, follow this proven three-step approach that our organization has refined through years of helping small businesses in Southern California.

Step One: Start with Your Bank

Your current bank should be your first stop. Many business owners don’t realize that banks have significantly streamlined their small business lending processes in recent years. Sometimes, all you need is a business credit line or a dedicated business credit card.

Why banks first?

- Regulated and transparent pricing

- An existing relationship may speed approval

- Often, the fastest route to working capital

- Clear repayment terms with no surprises

Yes, you’ll likely need to personally guarantee the payment, but this is often the most straightforward way to access capital for working expenses or new projects. If your banker says you don’t qualify or doesn’t offer business loans, don’t worry, move to step two.

Step Two: Explore Trusted Microlenders

If traditional banking isn’t an option, microlenders can be an excellent alternative. These organizations, often nonprofit organizations like our partners, receive funding from government agencies or foundations specifically to support small businesses.

Benefits of working with microlenders:

- Much more flexible than traditional banks

- Designed to help businesses build credit

- Simple application processes

- Focus on community development, not just profit

The process is typically straightforward: fill out an online form, maybe have a phone consultation, and you’re on your way. Microlenders are particularly helpful if you’re still building your credit or don’t have an extensive business income history.

To find reputable microlenders in our region, use the Small Business Assistance Tool to connect with someone who can help answer your questions.

Step Three: Get Professional Guidance

You don’t have to navigate this process alone. Business counselors at Women’s Business Centers, Small Business Development Centers, and other organizations that collaborate with us can provide invaluable support.

How business counselors help:

- Sharpen your financial management skills

- Develop strategies to boost sales and profitability

- Prepare your business for larger loans in the future

- Review loan offers and terms

- Connect you with trusted lenders in their network

Our research consistently shows that businesses receiving professional counseling are more likely to secure favorable loan terms and avoid predatory lending situations.

Essential Due Diligence Every Business Owner Must Do

Compare Multiple Offers

Never accept the first loan offer you receive. Always get quotes from at least three different lenders and compare:

- Interest rates and APR

- Origination fees and other costs

- Repayment terms and schedule

- Prepayment penalties

- Personal guarantees required

Demand Full Transparency

Request a detailed breakdown of all costs, including origination fees, insurance, taxes, and any other charges. You should know exactly what you’ll owe each month and over the life of the loan.

Read Every Line of the Fine Print

Never sign a loan agreement you don’t fully understand. Look specifically for:

- Negative amortization clauses (where your loan balance actually grows over time)

- Universal default provisions that can trigger penalty rates

- Automatic renewal clauses

- Cross-default provisions affecting other debts

Consider SBA-Backed Loans

SBA loans often provide lower rates, longer terms, and more borrower protections than conventional loans. While the application process may take longer, the additional protections and favorable terms are often worth the wait.

Building Financial Resilience: Lessons from the Pandemic

Our 2021 research revealed a crucial insight: businesses with strong financial management practices were far less likely to fall victim to predatory lenders during the COVID-19 crisis. Here’s how you can build that resilience:

Maintain Accurate Financial Records

The biggest barrier we observed to accessing legitimate funding was poor financial record-keeping. Businesses without current financial statements and proper bookkeeping often had no choice but to turn to predatory lenders.

Essential financial practices:

- Keep current profit and loss statements

- Maintain accurate balance sheets

- Track cash flow regularly

- Separate business and personal finances completely

Develop Multiple Funding Relationships

Don’t wait until you need money to build relationships with lenders. Establish connections with:

- Your primary business bank

- Local credit unions

- Community Development Financial Institutions (CDFIs)

- Reputable microlenders in your area

Create Financial Cushions

Build emergency reserves when times are good. Even a small cash cushion can prevent desperate borrowing during tough periods.

Resources for Inland Empire Business Owners

Government Resources

- FDIC Consumer Resource Center Money Smart: free financial education resources for consumers and small businesses

- FDIC BankFind Suite: a tool for consumers to identify federal regulators for their banks

- U.S. Small Business Administration: Comprehensive loan programs and lender matching services

- California Office of the Small Business Advocate: State-level support and resources

Local Support Organizations

- Our own Small Business Assistance Tool: A no-cost to low-cost business assistance tool to connect you to help and resources.

- Orange County Inland Empire SBDC Network: Business counseling and loan preparation assistance

- Inland Empire Women’s Business Centers: Specialized support for women entrepreneurs

Educational Resources

Our partners at CDC Small Business Finance have created an excellent toolkit to help you evaluate online lenders. Additionally, the SBA regularly publishes fraud alerts and scam warnings to keep business owners informed.

Take Control of Your Business’s Financial Future

Don’t let the pressure of needing cash push you into a deal that could destroy your business. Remember:

- Start with regulated, transparent lenders like banks and credit unions

- Explore reputable microlenders if traditional banking isn’t an option

- Get professional advice from business counselors and advisors

- Take time to compare offers and read all terms carefully

- Build strong financial practices to avoid desperate borrowing

The Inland Empire’s small business community is stronger when we all succeed. By choosing legitimate funding sources and building financial resilience, you’re not just protecting your own business; you’re contributing to a healthier economic ecosystem for everyone.